You probably type your credit card number a dozen times a month — into shopping carts, subscription forms, and app stores. But have you ever stopped to wonder what those 16 digits actually mean?

They are not random. Every single digit in your credit card number serves a purpose. Together, they tell a story: which network issued the card, which bank it belongs to, which account it is linked to, and whether the whole number is even valid. All of that is packed into 15 or 16 digits.

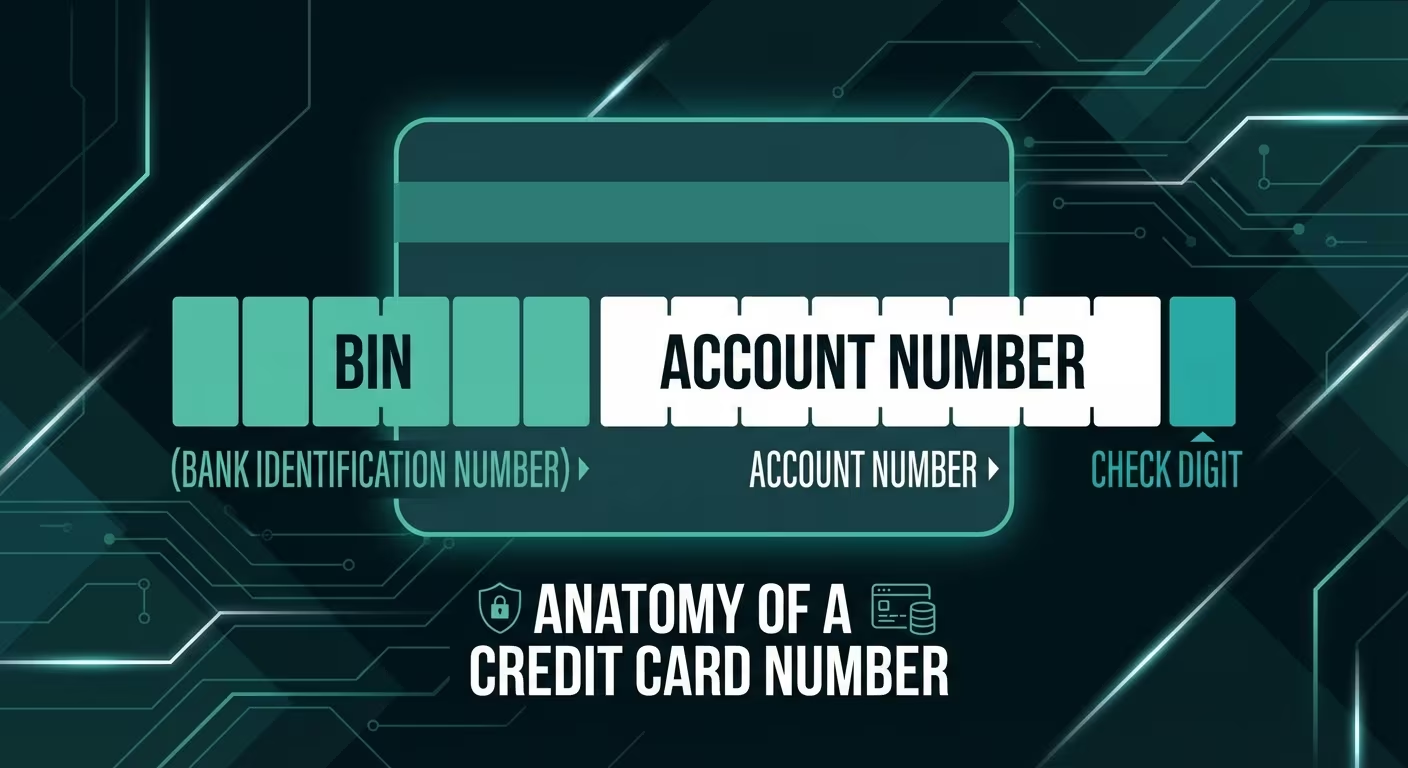

Let us break it apart.

The Structure of a Credit Card Number

A credit card number — technically called the Primary Account Number (PAN) — is typically 16 digits long (though Amex uses 15 and some cards use up to 19). It is divided into three sections:

| Section | Digits | Purpose |

|---|---|---|

| IIN / BIN | First 6-8 digits | Identifies the card network and issuing bank |

| Account Number | Middle digits | Unique to your individual account |

| Check Digit | Last digit | Validates the entire number using the Luhn algorithm |

Think of it like a phone number: the country code tells you which country, the area code narrows it to a region, and the remaining digits reach a specific phone. Credit card numbers work the same way — just with money instead of calls.

Section 1: The IIN / BIN (First 6-8 Digits)

The first section is called the Issuer Identification Number (IIN) — previously known as the Bank Identification Number (BIN). The industry officially switched to "IIN" in 2017, but most people (and most tools) still say BIN.

The First Digit: Major Industry Identifier (MII)

The very first digit tells you which industry issued the card:

| First Digit | Industry |

|---|---|

| 1 | Airlines |

| 2 | Airlines and financial |

| 3 | Travel and entertainment (Amex, Diners Club) |

| 4 | Banking and financial (Visa) |

| 5 | Banking and financial (Mastercard) |

| 6 | Merchandising and banking (Discover, UnionPay) |

| 7 | Petroleum |

| 8 | Healthcare, telecommunications |

| 9 | National assignment |

So when you see a card starting with 4, you instantly know it is a Visa. Starts with 5? Mastercard. Starts with 3? Could be Amex (37) or Diners Club (36, 38).

Digits 2-6 (or 2-8): The Issuing Bank

The remaining digits in the BIN identify the specific bank or financial institution that issued the card. For example:

- 4147 09 → Chase Visa

- 5425 23 → Capital One Mastercard

- 3742 45 → American Express

This is why BIN lookup tools exist — you can enter the first 6-8 digits of any card and find out which bank, country, and card type (credit, debit, prepaid) it belongs to.

Since 2022, the BIN length expanded from 6 to 8 digits for new issuances, giving room for more institutions as the global card market grows.

Section 2: The Account Number (Middle Digits)

The digits between the BIN and the check digit are your individual account identifier. This is the part that is unique to you — it links the card to your specific account at the issuing bank.

For a standard 16-digit card with a 6-digit BIN:

- Digits 7 through 15 = your account number (9 digits)

- That gives banks up to 1 billion unique account numbers per BIN

With the newer 8-digit BIN:

- Digits 9 through 15 = your account number (7 digits)

- That is still 10 million accounts per BIN — plenty for most issuers

Banks assign these numbers sequentially or using internal algorithms. The specifics are proprietary — each bank has its own system.

Section 3: The Check Digit (Last Digit)

The final digit is not part of your account number. It is a checksum — a mathematically calculated digit that validates the entire card number using the Luhn algorithm.

Here is the quick version of how it works:

- Starting from the right, double every second digit

- If doubling produces a number > 9, subtract 9

- Sum all the digits

- If the total is divisible by 10, the number is valid

The check digit is specifically chosen so that this calculation always produces a multiple of 10 for valid card numbers. It catches about 95% of single-digit errors and all transposition errors (swapping two adjacent digits).

How Card Numbers Differ by Network

| Network | Prefix | Length | Example |

|---|---|---|---|

| Visa | 4 | 13, 16, or 19 | 4242 4242 4242 4242 |

| Mastercard | 51-55, 2221-2720 | 16 | 5555 5555 5555 4444 |

| American Express | 34, 37 | 15 | 3782 822463 10005 |

| Discover | 6011, 644-649, 65 | 16-19 | 6011 1111 1111 1117 |

| UnionPay | 62 | 16-19 | 6200 0000 0000 0005 |

| JCB | 3528-3589 | 16-19 | 3530 1113 3330 0000 |

| Diners Club | 36, 38 | 14-19 | 3056 9309 0259 04 |

Notice that Amex uses a different grouping: 4-6-5 instead of the 4-4-4-4 pattern used by Visa and Mastercard. This is because Amex numbers are 15 digits, not 16.

Mastercard expanded their range in 2017 to include prefixes 2221 through 2720, giving them room for billions more card numbers as the original 51-55 range filled up.

Virtual Card Numbers

Modern banking has introduced virtual card numbers — temporary or limited-use card numbers that map to your real account but can be locked, limited, or deleted without affecting your physical card.

Services like Privacy.com, Apple Card, and many banks now offer virtual cards that:

- Can be locked to a single merchant

- Have spending limits

- Can be instantly closed

- Generate unique numbers for each subscription

The underlying mechanics are the same — virtual cards still follow the BIN + account + check digit structure. They are just generated on-demand and disposable.

Security: What Your Card Number Does (and Doesn't) Protect

Here is what most people get wrong: your credit card number is not a password. It is an identifier, like your phone number. Knowing someone's card number is necessary to charge them — but in modern payments, it is not sufficient.

Modern card security layers include:

- CVV/CVC: The 3-4 digit code on the back (or front, for Amex) that proves you physically have the card

- 3D Secure: A bank-side verification step (like a one-time SMS code) for online purchases

- Tokenization: Replacing the real card number with a disposable token for each transaction

- EMV chip: Generates a unique cryptogram for each in-person transaction

- Address Verification (AVS): Matching the billing address you enter with what the bank has on file

So while you should absolutely protect your card number, the industry has built multiple layers of defense assuming that card numbers will eventually leak.

Generating Test Card Numbers

Developers frequently need valid card numbers for testing payment integrations, form validation, and automated tests. Namso's card number generator creates numbers that:

- Follow the correct format for any card network

- Pass Luhn algorithm validation

- Use real BIN prefixes for realistic testing

- Are not connected to any real account

This is essential for testing payment gateways, building e-commerce platforms, and validating form inputs without risking real financial data.

FAQ

How many digits is a credit card number?

Most credit cards (Visa, Mastercard, Discover) use 16 digits. American Express uses 15 digits. Some card networks like Maestro can use 12-19 digits. The number of digits depends on the card network's standard.

Is the credit card number the same as the account number?

No. The credit card number (PAN) contains your account number as a subset, but also includes the BIN prefix and a check digit. Your bank account number and card number are different identifiers.

Can two credit cards have the same number?

No. Each credit card number is globally unique. Even if a card expires and a new one is issued, the new card typically gets a different number (though some banks keep the same number and only change the expiry and CVV).

What happens if someone knows my credit card number?

The card number alone is usually not enough to make purchases — most merchants also require the CVV, expiry date, and billing address. If your number is compromised, contact your bank immediately. Most banks offer zero-liability fraud protection.

Why do credit card numbers start with 4 or 5?

These prefixes identify the card network. Cards starting with 4 are Visa, and cards starting with 51-55 (or 2221-2720) are Mastercard. This system is part of the ISO/IEC 7812 standard that assigns number ranges to different industries and card networks.

Can I change my credit card number?

You cannot choose your card number, but you can request a new card with a new number from your bank. This is commonly done if your card is compromised or stolen. Your bank will issue a replacement with a different number linked to the same account.